Study: 29 U.S. municipal funds exposed to P.R. bonds

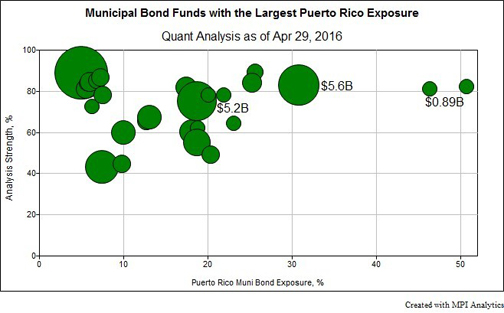

MPI’s chart depicts the size of the funds and their effective exposure to Puerto Rico; larger bubbles represent larger funds, some with more than a billion dollars’ worth of exposure in the case of a default.

As many as 29 out of 562 U.S. municipal bond funds currently carry an exposure to Puerto Rican bonds greater than 5 percent, some with an estimated exposure approaching 50 percent.

This assessment is based on research conducted by Markov Processes International, specialists in the systematic analysis of factors influencing investment performance, which provides analytics and reporting solutions to the financial services industry.

After Gov. Alejandro García-Padilla announced the possibility of further defaults, MPI analyzed the return streams of the 562 funds, examining all of the municipal bond categories in Morningstar using its factor-analysis tools.

“We wanted to fully understand how a possible Puerto Rico default would affect mutual funds investing in municipal bonds,” said Michael Markov, co-founder and chairman at MPI. “Investors should be as aware as possible where their funds are investing to understand the range and magnitude of factors that influence returns.”

“This is especially important in this low-yield environment when certain funds appear particularly attractive because of their higher yields. Since systematic factor-analysis isn’t relying on fund holdings, we can help identify risks in the absence of recent position data or when the use of derivatives or a large number of holdings makes positions hard to decipher,” he said.

Of the funds with high exposures to Puerto Rico, a few fund families had multiple funds, including Franklin Templeton, Goldman Sachs and Oppenheimer. According to Sean Ryan, a senior MPI research analyst, “while many municipal funds don’t have a detectable exposure to Puerto Rico, higher concentrations run in a few fund families. One municipal fund family has 17 of the 29 funds with high levels of exposure. A smaller fund has an exposure approaching 50 percent.”

MPI’s chart depicts the size of the funds and their effective exposure to Puerto Rico; larger bubbles represent larger funds, some with more than a billion dollars’ worth of exposure in the case of a default. For example, a large “5.6B” bubble is a fund with $5.6 billion in AUM, with a 31 percent exposure to the Puerto Rican index.

“Using MPI’s Dynamic Style Analysis, we analyzed a period of two years using daily analysis, comparing funds to two indices representing investment grade municipal bonds, one index representing high yield bonds and one Puerto Rican Bond index,” explains Markov. “Using a batch process, we ran regression analysis on all of the funds individually to identify those that showed an exposure greater than 5 percent to a Puerto Rican municipal bond index.”