Puerto Rico’s credit union industry strengthened by 20% increase in total deposits

Conditions for Puerto Rico’s credit union industry continued improving as of the fourth quarter of 2020, with greater liquidity, asset quality and a 20% increase in total deposits, according to the new Credit Union Industry Financial Stability Index for Puerto Rico, produced by Estudios Técnicos Inc. (ETI).

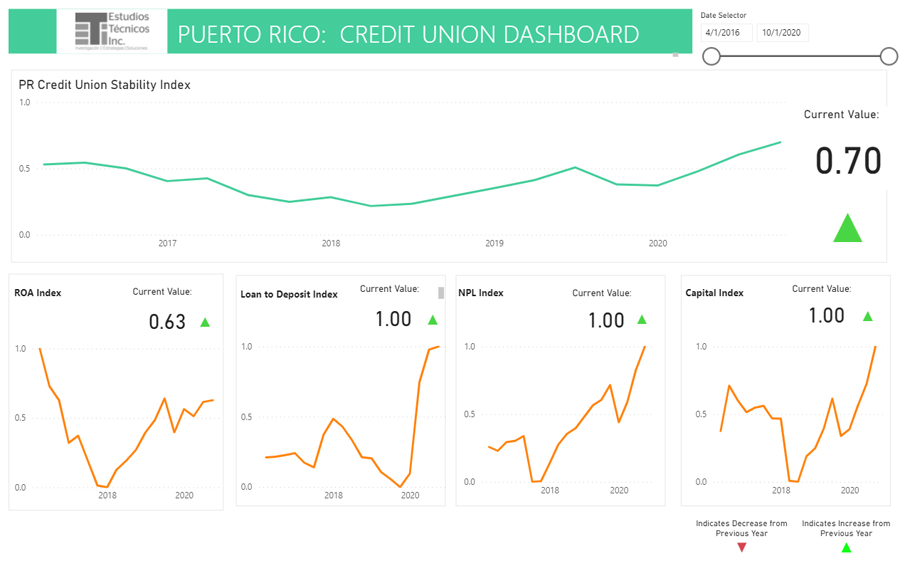

“The index increased from 0.38 in the fourth quarter of 2019 to 0.70 in the fourth quarter of 2020. During this period, the industry’s client base also rose by 30,075 to 1.08 million,” said ETI CEO Graham Castillo, who confirmed the firm will develop this index quarterly.

ETI also developed the Financial Stability Index for Puerto Rico’s Banking Industry, whose recent findings show that this industry’s liquidity and solvency remain strong despite the current economic environment.

However, due to differences in accounting principles applied by credit unions in Puerto Rico as compared to commercial banks, Castillo said the two indexes are not comparable.

“Both credit unions and commercial banks, components of Puerto Rico’s financial system, have shown significant improvement even with the very difficult conditions created by the pandemic,” he said.

Leslie Adames, director of the Economic Policy and Analysis Division at ETI, explained that the Credit Union Industry Financial Stability Index for Puerto Rico fluctuates between 0 (financial fragility) and 1 (financial strength).

It measures the financial health of the credit union industry with respect to four criteria: liquidity (total loans/deposits, or LtD), solvency (capital to total assets, or E/A), asset quality (nonperforming loans/total loans) and profitability (return on assets, or ROA).

Adames said the credit union industry’s liquidity strengthened, driven primarily by the flow of funds related to the COVID-19 fiscal stimulus. Total deposits rose 20% year-on-year to $10.3 billion in the fourth quarter 2020, while loan balances increased 0.21% year-on-year to $5.2 billion, leading up to an improvement in the loan to deposit ratio from 87.63% in the fourth quarter 2019 to 71.27% in the fourth quarter 2020.

The trend in asset quality also improved, with the credit unions’ nonperforming loans ratio falling from 3.18% to 2.71% during the period.

However, profitability remained under pressure affected by high expenses and lower interest margins. The expense ratio, which measures expenses relative to revenues, fell from 90.26% in the fourth quarter 2019 to 85.78% in the fourth quarter 2020, but remains high.

Negligible year-on-year loan balance growth, coupled with an 8-basis points reduction in loan yields to 7.33% in the fourth quarter 2020, continued affecting net interest margin despite lower cost of funds during the period, the firm stated.

Finally, total capital in the credit union industry, excluding stocks held by credit unions members, improved after falling 5.2% sequentially to $474 million in the fourth quarter 2019. Notwithstanding, the capital to total assets ratio fell from 5.7% in the third quarter 2019 to 5.01% in the third quarter 2020, driven by growth in cash balances and funds deposited in certificate of deposits, but improved to 5.16% in the fourth quarter of 2020.