US Dept. of Treasury grants 1-year transition period for taxpayers under Act 154

December 30, 2021

The US Department of Treasury and the IRS released the final regulations related to the Foreign Tax Credit under Act 154, which grants an additional transition year to taxpayers who currently pay under that tax ...

chat_bubble0 Comment

visibility1376 Views

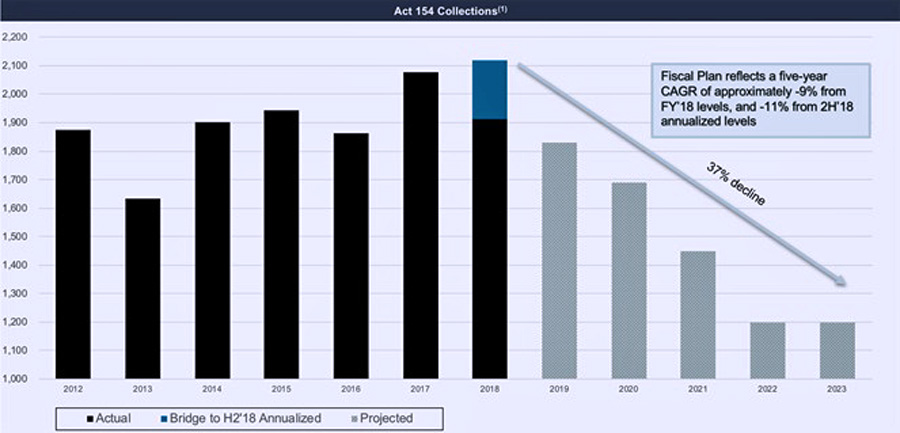

Op-Ed: Oversight Board includes arbitrary Act 154 assumptions in Fiscal Plan

December 5, 2018

Instead of using the most probable assumptions based on actual past results, the Oversight Board relied on untested assumptions which in combination arrive at extremely low expected revenue numbers for its projections.

chat_bubble0 Comment

visibility1047 Views

A Dow Jones/Factiva content provider since 2014