Op-Ed: P.R’s per capita debt load is ‘far lower’ than that of mainland states

January 17, 2019

Recent discussions of Puerto Rico’s debt levels by both Puerto Rico officials and the Financial Oversight and Management Board for Puerto Rico represent that the island’s per capita debt levels are far higher than the average per capita levels of mainland states in the U.S. mainland. However, that analysis compares only state-level debt and ignores […]

chat_bubble0 Comment

visibility1601 Views

Oversight Board, creditors’ committee challenge $6B of P.R. debt

January 15, 2019

The Special Claims Committee of the Financial Oversight Board for Puerto Rico announced that it and the Official Committee of Unsecured Creditors in Puerto Rico’s debt restructuring have filed an objection to more than $6 billion of Puerto Rico’s bonded debt. The objection asserts that the invalid debt was issued in clear violation of the […]

chat_bubble0 Comment

visibility1594 Views

Analyst: COFINA deal may usher in P.R.’s ‘next default’

October 31, 2018

If the prediction of zero economic growth by 2023 holds true, the deal with COFINA creditors will lead to a new default for Puerto Rico.

chat_bubble0 Comment

visibility2411 Views

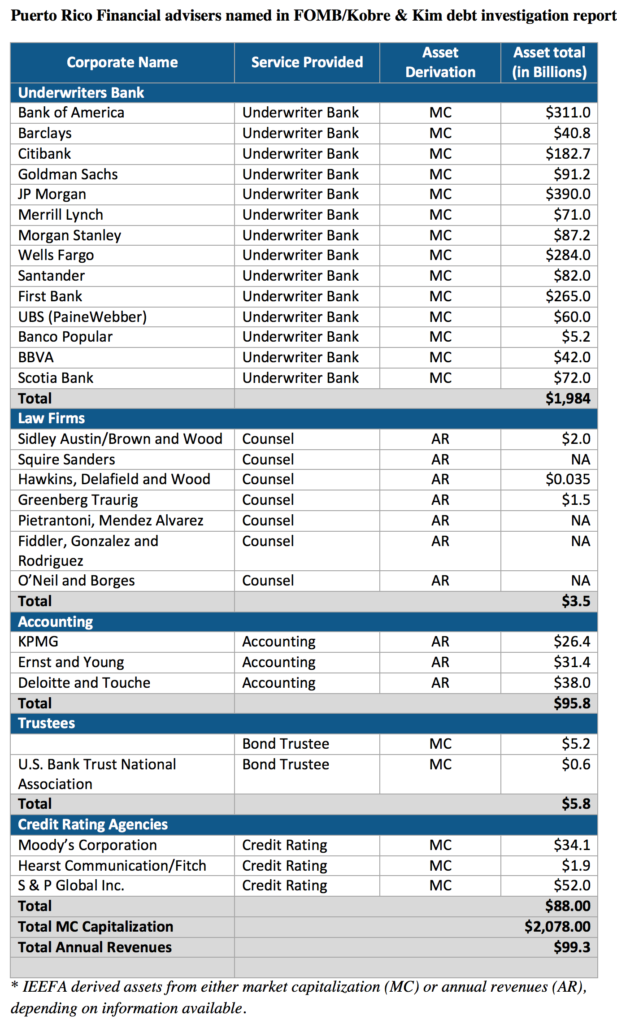

Op-Ed: The banks, law firms, accountants and credit agencies that orchestrated P.R.’s $72B debt crisis

September 5, 2018

Many of these same lawyers, accountants, bankers and credit-rating experts continue to have the ear of the Puerto Rican government.

chat_bubble0 Comment

visibility2235 Views

P.R. Oversight Board publishes debt investigation report, labels GDB debt ‘enabler’

August 21, 2018

The report, which is just under 600 pages long, includes the results of its investigation into Puerto Rico’s debt and its connection to the current fiscal crisis.

chat_bubble0 Comment

visibility3924 Views

OBoard, P.R. gov’t reach deal with COFINA creditors; to save $17B+ in debt service

August 9, 2018

The Financial Oversight and Management Board for Puerto Rico and the government of Puerto Rico announced they have reached a deal with Senior and Junior bondholders of Sales Tax Financing Corp. credit, as well as monoline insurers.

chat_bubble0 Comment

visibility2469 Views

P.R. debt audit drags on as creditor negotiations heat up

June 12, 2018

A mural alongside Baldorioty de Castro Avenue in San Juan, near the exit to De Diego Street, reads nowadays, “¡Auditoría ya, mamabichxs! A ciegas no” (which roughly translates into “Audit Now, suckers! Don’t do it blindly.”)

chat_bubble0 Comment

visibility2577 Views

Assured Guaranty: P.R.’s latest fiscal plan projects $6B surplus

March 29, 2018

Puerto Rico had greater financial resources than it previously claimed, but there continues to be little transparency in the process, and audited financial statements still have not been produced since 2014, said Dominic Frederico, CEO of Assured Guaranty Ltd., which holds government debt.

chat_bubble0 Comment

visibility2028 Views

Op-Ed: Debt forgiveness and tax considerations

March 6, 2018

In upcoming years, the term “debt forgiveness” will become a common phrase among individuals, proprietorships, and businesses in Puerto Rico, but not for a good reason.

chat_bubble0 Comment

visibility3552 Views

Study: No new growth strategy will work without debt restructuring

January 17, 2018

Before Hurricane María, if Puerto Rico were to pay off its debt without completely choking off economic and social development, it needed a total cancellation of the interest on the public debt and a reduction in the principal of approximately 45 percent to 90 percent. Now, in the wake of the storm, the debt relief needed is much greater.

chat_bubble1 Comment

visibility2382 Views

Moody’s: Delay in P.R.’s fiscal plan underscores growing economic uncertainties

January 13, 2018

The Commonwealth of Puerto Rico's second delay in submitting its revised fiscal plan to the Financial Oversight and Management Board for Puerto Rico "underscores the growing economic uncertainties it faces as it continues to recover from Hurricane María," Moody's Investors Service noted in a new report.

chat_bubble0 Comment

visibility1569 Views

National voluntarily dismisses complaint vs. PREPA

October 16, 2017

National Public Finance Guarantee Corporation announced that it and other creditors have voluntarily dismissed without prejudice the adversary complaint filed on Aug. 7, 2017 which sought to compel the Puerto Rico Electric Power Authority to deposit revenues with the bond trustee as required by the terms of the PREPA Trust Agreement, PROMESA and the U.S. Constitution.

chat_bubble0 Comment

visibility1850 Views

PR debt insurers pull court complaints against fiscal plan

October 7, 2017

In what could represent the first positive for Puerto Rico in its litigation with creditors and insurance companies over debt repayment, two monoline insurers — National Public Finance Guarantee Corp. and Assured Guaranty withdrew their complaints against the Commonwealth’s Fiscal Plan.

chat_bubble0 Comment

visibility2361 Views

PR’s debt payments could be reduced to 0, for now

October 3, 2017

Puerto Rico’s debt service payment could be reduced to zero in the short-term, when the Financial Oversight and Management Board for Puerto Rico modifies the fiscal plan to readjust it to the island’s new panorama following the humanitarian crisis provoked by the passage of a category 4 hurricane through the island.

chat_bubble0 Comment

visibility2190 Views

Moody’s: Hurricane Irma further cripples PREPA

September 13, 2017

Hurricane Irma will have negative implications for the Puerto Rico Electric Power Authority’s liquidity and cause further delays to its debt restructuring plans, Moody’s Investors Services predicted in a report released Tuesday.

chat_bubble0 Comment

visibility1858 Views

A Dow Jones/Factiva content provider since 2014

NIMB ON SOCIAL MEDIA