Op-Ed: P.R. banking sector fully transformed in 10 years

In the past 10 years, the size of the local economy has shrunk by 14 percent, total employment has dropped by 21 percent (more than 250,000 jobs) and the total population has decreased by 9 percent. The deterioration of the PR economy has taken its toll on the banking system.

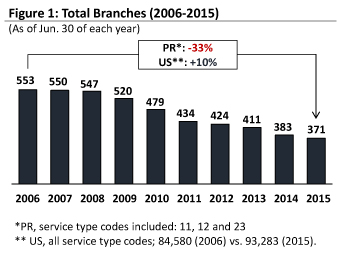

Since December 2015, the number of retail banks has reduced from 10 to five, the number of branches has decreased from 553 to 371 (33 percent drop), total banks’ employees have reduced by 2,800 (18 percent drop), and total banking assets have decreased by $42 billion (42 percent drop). During the same period of time, total banking assets increased by 35 percent in the United States (see Figures 1 and 2).

The financial difficulties of Puerto Rican families and businesses have also resulted in higher delinquency levels and credit losses for the banking industry. While noncurrent loans and leases represented around 2 percent of total loans and leases in the 2002-2005 period, they jumped above 10 percent every single year between 2009 and 2012. Delinquency has improved since 2012, but remains substantially above both mainland and Puerto Rico pre-crisis levels.

The financial difficulties of Puerto Rican families and businesses have also resulted in higher delinquency levels and credit losses for the banking industry. While noncurrent loans and leases represented around 2 percent of total loans and leases in the 2002-2005 period, they jumped above 10 percent every single year between 2009 and 2012. Delinquency has improved since 2012, but remains substantially above both mainland and Puerto Rico pre-crisis levels.

The credit losses incurred by local banks have translated into a significant deterioration of their profitability. The pre-tax return on equity (ROE) of the local banking system averaged 17 percent during the 2002-2005 period. Between 2006 and 2015, the average pre-tax ROE reduced to 1.4 percent, dropping to approximately -10 percent in 2009 and 2010.

On the other hand, the past 10 years have seen a dramatic improvement in the solvency and liquidity of the banking system. The stricter oversight of federal regulators and the Dodd-Frank reforms have translated into larger capital requirements to comply with more stringent stress tests. The industry’s Tier 1 risk-based capital ratio increased from 10.6 percent in 2006 to 18.6 percent at the end of 2015, significantly above the well-capitalized level as defined by the FDIC.

The change in funding mix in the past 10 years also shows the magnitude of the banking sector transformation. The domestic deposits to total assets ratio increased from 56 percent in 2006 to 76 percent in 2015. Meanwhile, brokered deposits to total deposits reached 44 percent in 2008 and dropped to 10 percent by 2015. The use of brokered deposits was key in the 1990s-2000s to finance the Island’s real estate bubble, which explains the pressure imposed by the FDIC to reduce the dependency of this funding source by local banks.

The banking sector today shows a healthier balance sheet and a more robust capital position to face additional economic and financial turmoil in the coming years.

In summary, the banking sector today shows a healthier balance sheet and a more robust capital position to face additional economic and financial turmoil in the coming years. The pain so far has been shared by local banks through higher credit losses and lower profitability, and by the FDIC insurance fund with an estimated impact of $5B to absorb part of the losses incurred in the failure of R-G Premier Bank, Westernbank and Eurobank in April 30, 2010 and Doral Bank in February 27, 2015.

Looking forward, Puerto Rico’s economic and fiscal outlook for 2016 is grim at best. The GDB’s economic activity index (GDB-EAI) continues its downward trend, and economic growth projections of the government (Base projection of FY 2016: -1.2 percent) and private sector economists are dismal. The government is expected to continue to default on its debt obligations and be forced to make additional spending cuts and/or tax increases to eliminate its chronic fiscal deficit. This will likely further depress consumer and business confidence in an already frail economy.

Although it is unclear how exactly these adverse trends will impact the local banking sector, we should not expect a reduction of delinquency and charge offs in the near future. Assets, and loans and leases portfolios in particular, will likely continue to decrease due to credit losses, the regular amortization of loans and lower loan refinancing and originations.

This, in turn, will further reduce the revenue and profit generating capacity of the banking sector. There will likely be pressure from investors and shareholders to increase profitability through more cost rationalization measures given the persistently high credit losses, a lower revenue generating asset base and larger capital levels.

Banks will continue to look for opportunistic portfolio acquisitions to offset the reduction of their asset base. Further consolidation is also likely, but given that Banco Popular and FirstBank already control approximately 2/3 of the local banking business, there may be concerns about market concentration from local and federal regulators. Geographic diversification will continue to make sense for Popular, FirstBank and Oriental given their high level of dependence in the PR market.

In summary, this 10-year review of the local banking sector makes it evident that the Puerto Rico banking sector still has a long way to go before seeing pre-2006 profitability levels. Banks need to continue reducing their exposure to bad debts, not only from the private sector but now also from government (i.e central, public corporations and municipalities) loans and investments. Competition within the sector will become increasingly intense, given the reduced number of banks fighting for market share in a shrinking economy.

Furthermore, given the limited opportunities in the local market and strong loan growth in U.S. markets, identifying and seizing opportunities in nonlocal markets will be more important.

Nevertheless, the historically high capital levels of local banks will help protect their financial stability and economic viability in case of even more adverse economic and fiscal conditions.

To access the full V2A Puerto Rico Banking Industry Report, click HERE.

Banks are unable to function in Puerto Rico and that has compounded the problem further. Puerto Rico’s real estate assets have become so devalued that real estate funds from the US are unable to resist the opportunities to purchase all cash deals in Old San Juan, Condado and Isla Verde. In these nice areas there are no more good deals. If you go outside the three above mentioned locations you may still pick up a good properties for a huge discount, but do not expect any bank to jump on the opportunity to give you a loan. They can barely keep up with the regulators. Puerto rico needs Bank of America, JP Morgan Chase, Citibank and Wells fargo and then let me tell you that it will be a come back as good as the one we’ve seen in the US. Sadly that will not happen because local banks will collapse, since they will be unable to compete. There are still so many foreclosed homes and defaulted borrowers in the system that Puerto Rico will need at least another 5 to 7 years to start seeing some aggressive moves by local banks to give good loans to good buyers. For some this is the opportunity of a life time, for most, it is an absolute disaster!