Banking exec: Gov’t must act with ‘conviction, urgency’

Oriental CEO José Rafael Fernández

The Puerto Rico central government is facing pressure to “act with more conviction and with more urgency” to address its dwindling liquidity, crushing debt and anxiety building up over the island’s fiscal problems, local banking executives said.

José Rafael Fernández, CEO of Oriental Financial Group told industry analysts during an earnings call on Friday that to begin turning things around, the government’s actions should address two aspects: “commit to execute a credible plan to reduce spending and increase competitiveness; and two, bondholders need to be convinced that Puerto Rico has the will to do so.”

“With this in mind, we urge government officials to recognize the impact the current uncertainty is having on the overall business climate in Puerto Rico,” he said.

Saying that Puerto Rico’s self-proclaimed inability to pay off its $73 billion public debt has generated “more anxiety outside of Puerto Rico than the situation warrants,” Fernández noted that even in the most severe scenario, Oriental “remains well above regulatory capital requirements and above the market cap range in which we have been trading.”

Oriental, as well as Puerto Rico’s largest bank, Banco Popular, is exposed to the government’s debt, as both have extended credit facilities to public agencies and municipalities.

As of June 30th, Oriental’s loan exposure to the central government totaled $301 million, down 21 percent from $380 million at March 31.

The largest loan is a contractual obligation with the Puerto Rico Electric Power Authority, a non-taxable $200 million fueled purchase line of credit, part of a syndicated $550 million line acquired when it bought BBVA last year.

“It is the most senior PREPA debt, and has payment priority over the government’s utilities, other credit obligations. Even though we placed this loan on non-accrual in the first quarter of 2015, we continue to receive interest payments. Interest payments during the second quarter dropped down the principal balance to $197.6 million,” Fernández said.

“It is important to note that the PREPA loan syndicate is now engaged in active discussions to arrive at a consensual negotiation to term out our credit facility. This is completely different from the situation last quarter, when PREPA had demonstrated an unwillingness to engage in a constructive dialog,” he said,

The executive added that the bank is hopeful that negotiations will reach a satisfactory conclusion by Sept. 1, as established by the forbearance agreement between bondholders and PREPA to address the agency’s $9 billion debt.

Meanwhile, Oriental confirmed its outstanding $100 million loan with the Puerto Rico Aqueduct and Sewer Authority was paid off June 1. The Puerto Rico State Insurance Fund has a $78 million loan with the bank, which is collateralized 130% percent by a portfolio of eight plus or better rated securities, pledged and held in an account at JP Morgan Chase in New York.

“This agency is not part of the government’s plan to negotiate bond terms, and the loan is well secured,” Fernández said.

Oriental has a $25 million loan in a long-term credit facility to the Puerto Rico Housing Finance Authority. It is repaid from inactive and unclaimed customer deposits from local financial institutions.

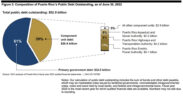

“We started disclosing our exposure to the Puerto Rico central government and public corporations in the third quarter of 2013. At that time, our exposure was $772 million. Today, that exposure has been reduced to $322 million,” Fernández said, noting it represents close to a 60 percent reduction.

Oriental also has $240 million in loans to five Puerto Rico municipalities, which are separate from that of credit related to the Puerto Rico central government and its public corporations.

“These loans do not share the same credit characteristics. These municipalities are autonomous from the central government and its agencies, which have a higher debt load and have grabbed headlines with the governor’s recent statements,” Fernández said, adding the individual loans are underwritten under its own credit policy, and are not traded as municipal paper in the market.

“We cannot control what the Puerto Rico central government will do in their negotiations with their bondholders. So our strategy is to approach the next few quarters cautiously, continuing to seek opportunities to further de-risk the balance sheet, and as an example, reevaluating alternatives to dispose covered non-performing commercial loans,” Fernández said. “And of course, we will continue to closely monitor our PREPA exposure as well.”

Popular Inc. CEO Richard Carrión

Popular offers helping hand

In a separate investor call, Richard Carrión, CEO of Popular Inc., parent company of Banco Popular, said the majority of its direct Puerto Rico government exposure is in loans to municipalities not publicly traded securities.

“Our direct exposure is down $266 million for the previous quarter and down to $104 million compared to last year’s second quarter as some balances were paid down to deferred tax a year,” he said. “However we will continue to collectively participate in funding the Puerto Rico government’s capital needs where we feel that risk reward is in our favor.”

Carrión also said the bank is willing to help the government execute its five-year fiscal stability plan, one of several steps Gov. Alejandro García-Padilla tasked its work group to draft by Aug. 30.

“We hope that the political leadership will arrive at solutions that will achieve fiscal balance and, more importantly, put the economy back on the growth track,” Carrión said. “We will do everything in our power to support this result.”