Puerto Rico’s banking industry reflects strength in liquidity, capital

The Financial Stability Index for Puerto Rico’s banking industry, prepared by Estudios Técnicos, Inc. (ETI), shows that the industry’s liquidity and solvency remain strong despite the current economic environment.

“The financial stability index for Puerto Rico’s banking industry has recovered after declining from 0.64 in the fourth quarter of 2019 to 0.54 in the first quarter of 2020. As of the fourth quarter of 2020, the index stood at 0.57,” said Leslie Adames, director of the Economic Policy and Analysis Division at ETI.

“The index, which fluctuates between 0 (financial fragility) and 1 (financial strength), has been improving in recent quarters, reflecting the strengthening of local banks’ liquidity, largely attributable to the inflow of federal stimulus funds related to the COVID-19 pandemic. The inflow of these funds implies a significant injection of liquidity for local banks,” he said.

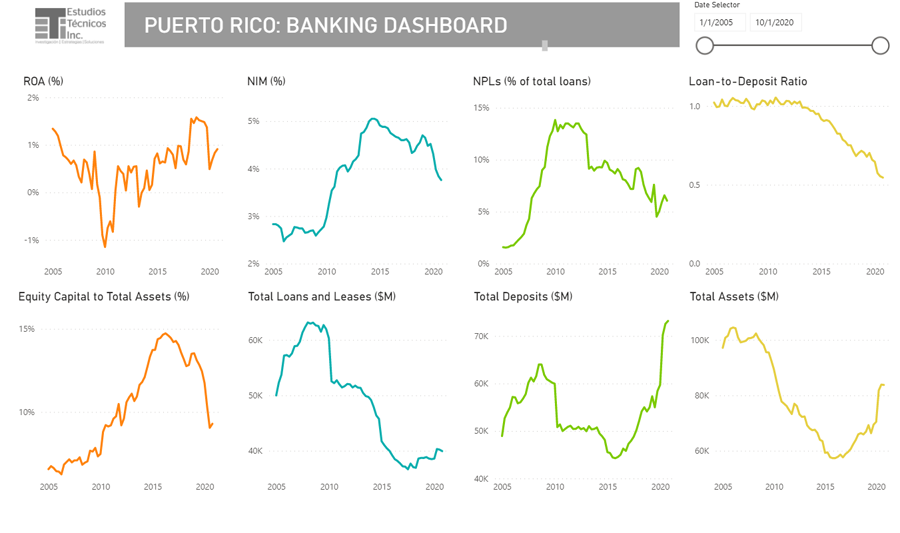

ETI developed the Index to measure the financial health of the island’s banking industry based on four indicators: liquidity (total loans/deposits), solvency (equity to total assets), asset quality (nonperforming loans/total loans) and profitability (return on assets or ROA), said EIT President Graham Castillo.

He noted the strength on the liquidity side by saying that “total deposits increased 25% year-on-year to $73.2 billion in the fourth quarter of 2020, while loan balances rose 3.7% from the prior year to $39.9 billion.

This resulted in a strengthening of the Loan-to-Deposit ratio from 65.88% in the fourth quarter of 2019 to 54.58% in the fourth quarter of 2020.

Castillo pointed out that “to receive the pandemic aid, people needed to have a deposit account in a depository institution, something that contributed to the recent upward trend in deposit balances.”

Adames agreed on this assessment noting that “compared with 2009-2010, and despite the reduction in the number of banks operating in the island from eleven to three entities, the industry is nowadays in a more solid position in terms of capital and liquidity.”

A challenge for the sector is the compression in net interest margin.

“This compression in margin responds to the low interest rate environment, which is affecting interest spreads and, consequently, the interest income generated from banks’ loan portfolios.” said Adames.

He explained that due to the current economic environment, banks had to implement stricter loan origination policies, affecting loans originations.

In addition, “banks have been deleveraging their balance sheet, that is, their loan portfolio balance has been declining over time, affecting the yield on loan portfolios… You have a smaller balance and lower interest rates, generating compression in interest margin,” Adames said.

Consequently, banks are taking measures to offset this situation by improving efficiency through reduction in operating costs and improvement in processes.

According to the banking index, “although the capital to total assets ratio has fallen sequentially since the second quarter of 2019, regulatory capital ratios remained above the minimum required by the Federal Deposit Insurance Corporation to be well-capitalized,” he said.

The industry’s Common Equity Tier 1 was 15.81% and the Leverage Ratio 8.61% — metrics well above 6.5% and the 5.0% minimum regulatory threshold required by the FDIC — for the fourth quarter of 2020, suggesting that local banks have sufficient capital to absorb potential losses and continue operating as a going concern,” Adames said.

Meanwhile, Castillo said the ETI’s interdisciplinary team of consultants together with its Data Analytics division, will continue to develop indexes for different sectors of the economy, which the public will be able to access free of charge on the firm’s website.