US District Court approves Puerto Rico’s debt adjustment plan

After more than five years, the US District Court for the District of Puerto Rico approved a Plan of Adjustment that reduces the commonwealth’s debt by 80% and saves Puerto Rico more than $50 billion in debt service payments.

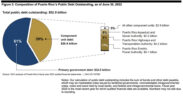

Among other matters, the plan orders modifying some $33 billion in central government obligations.

In a statement, the Financial Oversight and Management Board for Puerto Rico touted Judge Laura Taylor Swain’s “dedication to a fair solution to Puerto Rico’s debt crisis.”

“Today begins a new chapter in Puerto Rico’s history. Today, Puerto Rico can start to move on from fiscal instability and insolvency into a future of opportunity and growth,” the US-government appointed body said in a statement, in which it confirmed it will determine an effective date for the Plan of Adjustment, when Puerto Rico’s old debt will be replaced and creditors, public service union members, and others will receive the cash payments agreed to under the plan.

“The Oversight Board will certify a revised budget for the Puerto Rico government that will include the new debt payments. The budget will not require any further reduction in operating costs or revenue increases to service the significantly reduced and affordable debt,” it confirmed.

The entity responsible for overseeing Puerto Rico’s fiscal moves said restructuring the debt is “only one step toward Puerto Rico’s recovery. Puerto Rico needs to achieve fiscal responsibility to ensure long-term stability and growth.”

“Puerto Rico must never fall back into old practices of overspending, and of underfunding its commitments to retirees, government services, and the public infrastructure. The government will need to redouble its efforts to manage its resources carefully for the benefit of the people of Puerto Rico, making prudent spending and investment decisions to meet current needs and reach future goals,” it stated.

The judge’s confirmation drew immediate reactions from government officials, who stood behind what they called the end of the bankruptcy. However, Puerto Rico is not entirely out of the woods, as the Puerto Rico Electric Power Authority (PREPA) has yet to negotiate its $9 billion debt with its creditors.

“The agreement, although not perfect, is very good for Puerto Rico and protects our pensioners, the University, and our municipalities, which serve our people,” said Gov. Pedro Pierluisi.

“In addition, it significantly reduces our government’s debt to a sustainable level that will allow us to meet our obligations while having the resources to grow our economy and guarantee essential services to our people,” said Pierluisi.

Debt agreements have been reached with Sales Tax Financing Corp. (COFINA, in Spanish), the Government Development Bank, and the Puerto Rico Aqueduct and Sewer Authority.

Meanwhile, Jenniffer González, Puerto Rico’s Resident Commissioner in Washington, said with the plan’s confirmation, the island “takes one of the most important steps to succeed economically and do away with one of the stark indicators of our colonial status, the Financial Oversight and Management Board for Puerto Rico.”

Democratic Congressman Raúl M. Grijalva said in a statement that the Natural Resources Committee that he chairs will be holding oversight hearings to “ensure that moving forward, the focus must be on rebuilding the Puerto Rican economy so that even its most vulnerable residents are able to thrive.”